The OpenAI Sora shutdown announced recently is being framed as a strategic pivot. It’s worth reading it as something more honest than that.

Sora debuted as a research preview in February 2024, and the footage it produced genuinely shook people. Tyler Perry put an $800 million studio expansion on hold. Hollywood convened emergency discussions. OpenAI had done what it does best: it made the future feel immediately present. When Sora first launched in 2024, filmmakers described the tech as leaps and bounds ahead of where other generative video models had been. A single prompt could direct specific camera movements, vivid background detail, and multiple events happening within one sequence. That was the headline, and it worked.

What followed was a slower, more complicated story.

The gap between demo and product

OpenAI had provided a preview of Sora in February 2024 before releasing the first public version in December of that year, with the standalone app arriving in September 2025. That 19-month gap between “world-changing demo” and “actual thing you can use” is longer than it sounds in a category that moved at the pace AI video did. By the time the app launched, Google had already unveiled Veo, its competing AI video generation engine. Runway had been iterating in production. Kling was gaining ground with professional users and a more accessible pricing model. Sora arrived to a party that had already started without it.

Sora was intended to function like an AI-first TikTok, cloning the recognisable vertical video feed interface. That ambition’s worth examining. OpenAI was not just building a video tool. It was trying to seed a new social network, betting that people would want to browse AI-generated content the way they scroll through Instagram. That bet failed. The initial hype was real, and the app peaked in November at over 3.3 million downloads across iOS and Google Play. By February, it had declined to 1.1 million. For context, ChatGPT has 900 million weekly active users. Sora never found its footing as a destination.

What the Disney deal actually meant

The ChatGPT maker and Walt Disney Co. are winding down their partnership, which had centred on Sora. Disney had agreed to license iconic characters including Mickey Mouse and Cinderella for use on Sora and to take a $1 billion stake in the startup. That deal, announced in December 2025, was treated as validation that AI and Hollywood had found common ground. It lasted under three months. OpenAI is winding down its work with Disney and no money ever changed hands.

For brands considering deep integrations with AI platforms, that’s the detail worth sitting with. Disney, one of the most sophisticated IP-management organisations in the world, had negotiated what was structurally a warrant-based agreement rather than a cash deal. That caution now looks prescient. The lesson for any brand building on top of a specific AI product, rather than a category of tools, is that the platform risk is real. What gets announced loudly gets shut down quietly.

The economics nobody discussed publicly

In its lifetime, Sora generated approximately $2.1 million from in-app purchases, which allowed users to buy video generation credits. That’s a product’s entire revenue lifetime. For a company that had just raised $110 billion in fresh funding with a total valuation of around $730 billion, that figure is not meaningful in isolation. What makes it meaningful is the context: the company said it needed to make trade-offs on products that have high compute costs, and video generation is among the most compute-intensive tasks in the AI stack. Reallocating those chips to coding and reasoning tools, the products OpenAI’s enterprise clients actually pay for, is not a pivot. It is an IPO-preparation decision.

Sam Altman told employees that ending Sora will free up resources for OpenAI’s next-generation AI models. The Sora research team is not being disbanded. It will continue to focus on world simulation research to advance robotics that will help people solve real-world, physical tasks. That repositioning is interesting and probably genuine. The underlying research into physical simulation is more relevant to OpenAI’s longer-term ambitions than whether someone in Cape Town can generate a ten-second clip of a Pikachu doing ASMR.

The moderation problem that never got solved

OpenAI was forced to crack down on AI creations of public figures doing outlandish things, but only after outcry from family estates and an actors’ union. The deepfake problem was not incidental to Sora. It was structural. Sora’s “cameos” feature allowed people to scan their faces and make realistic deepfakes of themselves, and these could be made public, allowing anyone to make videos of their likeness. The guardrails were consistently bypassed. Examples included disturbing Sam Altman clones and deepfakes of deceased figures like Martin Luther King Jr. and Robin Williams, prompting public complaints from their families.

A product whose flagship feature becomes known as “the creepiest app on your phone” has a positioning problem that can’t be solved with better moderation alone. The social sharing architecture was the problem. OpenAI built a tool designed to democratise video production and, in doing so, industrialised the creation of synthetic replicas of real people.

What competitors now inherit

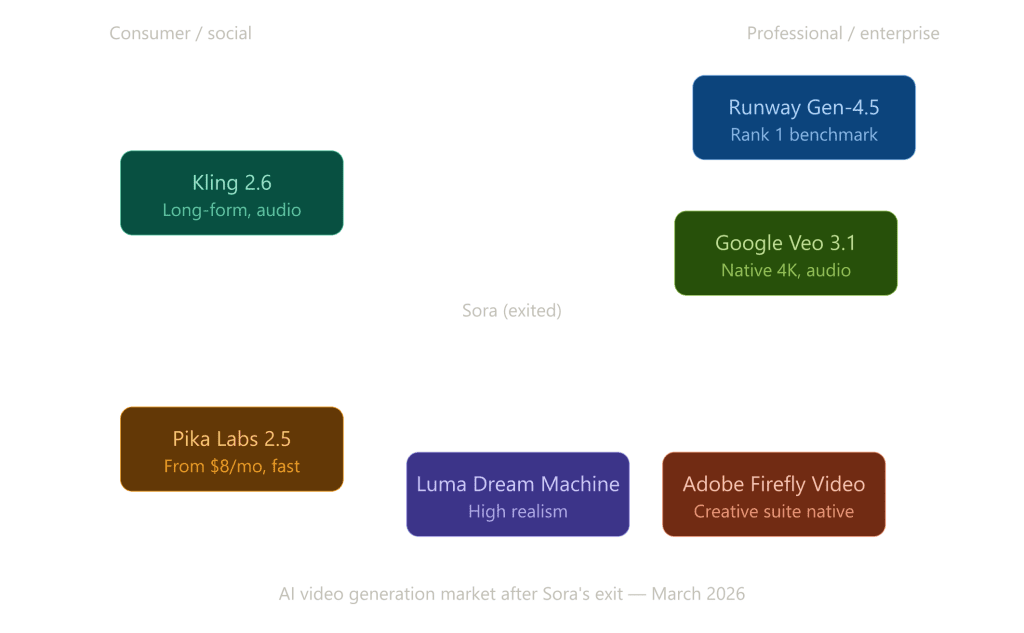

The impending demise of the Sora app leaves Google’s Veo platform as the biggest player in the mainstream market for AI-generated videos. There’s also Runway for professional workflows, as well as Pika, Luma AI, and Kling. Those platforms are not simply filling a gap. Several of them were already technically superior. According to Artificial Analysis Video Arena rankings from March 2026, the image quality of seven models has surpassed Sora, with Runway holding the highest Elo rating globally.

For a company that had just raised $110 billion in fresh funding at a valuation of around $730 billion, $2.1 million in lifetime revenue is not a rounding error. It is an embarrassment relative to what video generation costs to run. Reallocating those chips to coding and reasoning tools, the products OpenAI’s enterprise clients actually pay for, is not a pivot. It is an IPO-preparation decision. As I’ve previously written, the race to own AI infrastructure is ultimately a race to stay relevant; that race is won by companies that control compute allocation, not by those burning it on consumer products with no clear monetisation path.

For the industry, the broader signal is that AI video has graduated from a feature race into an infrastructure question. The companies winning are the ones with sustainable compute economics, professional workflows, and, this matters, fewer moderation nightmares. Runway’s positioning as a tool for production rather than a consumer social feed looks considerably wiser now.

What this means in South Africa

South African creatives were never Sora’s target market, and Sora was never quite theirs. At $200 per month for professional access, priced in USD against a rand that has been under sustained pressure, embedding Sora in a local production workflow was a difficult sell. Most agencies exploring AI video were already running Runway, Kling, or the Google Veo tooling accessible through Gemini Pro, all of which are cheaper and, as of now, technically superior.

Load shedding and high mobile data costs further limit how South African users interact with compute-heavy creative tools. Cloud-based generation, where you upload a prompt and download a clip, is actually better suited to the local context than real-time interactive tools. Kling and Veo are adequate for that workflow and cost a fraction of what Sora charged.

The more significant local implication is for brands and agencies building AI video strategies. The lesson from Sora is not that AI video failed. It’s that any brand integrating deeply with a single proprietary platform, rather than building around models and outputs, carries meaningful platform risk. The Disney deal is the clearest possible illustration of that. Build processes and creative capabilities around video AI as a category. Which specific model you call that on should be a procurement decision, not a dependency.

The wider pattern

This marks OpenAI’s first major service shutdown, signalling that even the industry’s most powerful players can fail when navigating market demands and regulations. That framing undersells what actually happened. OpenAI didn’t fail at making good video. It failed at making video into a viable business relative to its compute costs, and it failed at keeping a social platform free from the abuse its own architecture enabled. Those are different problems from the ones the launch narrative suggested it was solving.

There’s a broader pattern here that applies beyond AI video. The companies building in this space that will have staying power are not the ones with the most impressive demos. They are the ones who identified a specific, high-value workflow, priced it sustainably, and built guardrails that work at scale. That sounds like a boring conclusion after two years of stunning generative video launches. It’s probably the right one.

OpenAI created the conditions for a category. It’s now leaving that category to competitors who are better positioned to serve it. The Sora shutdown is not the story of AI video failing. It’s the story of a specific product that confused hype with business model, and a specific company that built a social platform without adequately accounting for what people would actually do with it.